Getting a mortgage in retirement can feel like an uphill battle. You have excellent credit and plenty of savings, but because you don’t have a W-2 paycheck, many traditional banks view you as “unemployed.”

You don’t need a job to get a loan; you just need a lender who understands retirement income.

Not all lenders are created equal. Some strictly follow “the box” and will reject you. Others specialize in “Asset Depletion” and “Social Security Grossing Up”—methods that allow you to use your nest egg to qualify for a loan easily.

As your trusted advocate, we have vetted the market to find the 5 best lenders who cater specifically to the financial profile of a retiree.

Key Takeaways

- The Criteria: We prioritized lenders that offer Asset Depletion (using savings as income) and have dedicated loan officers for complex income.

- Best Overall: Guaranteed Rate wins for its flexible underwriting and digital ease.

- Best for Service: Rocket Mortgage offers 24/7 support and seamless integration with investment accounts for income verification.

- The Strategy: Always tell the loan officer upfront: “I am retired and need to qualify using asset depletion or retirement income.”

Quick Comparison: Top Lenders for Seniors

We rated these companies based on their underwriting flexibility and ease of use for retirees.

|

Lender

|

Sagewise Rating

|

Best For

|

Key Senior Benefit

|

|---|---|---|---|

|

Guaranteed Rate

|

5.0 / 5.0

|

Asset Depletion

|

Flexible rules for using 401(k) balances as income.

|

|

Rocket Mortgage

|

5.0 / 5.0

|

Technology

|

Links to your bank to verify assets instantly (no paper chasing).

|

1. Best Overall: Guaranteed Rate

Sagewise Rating: 5.0

- Why it wins: Guaranteed Rate has established itself as a leader in “non-qualified” mortgages. They understand that a retiree’s wealth is often in assets, not monthly salary. Their proprietary “Grater” technology simplifies the application process, but they back it up with human loan officers who specialize in complex income structures.

- The Senior Benefit: They are experts at Asset Depletion. If you have $500,000 in an IRA but only draw $1,000/month, traditional banks might reject you. Guaranteed Rate can mathematically convert that $500,000 portfolio into a “qualifying monthly income” (often using a calculation like Total Assets / 360 Months), helping you qualify for a much nicer home without needing a job.

2. Best for Simplicity: Rocket Mortgage

Sagewise Rating: 5.0

- Why it wins: Retiring involves enough paperwork; your mortgage shouldn’t add to it. Rocket Mortgage (formerly Quicken Loans) has the best digital interface in the industry. Their “Rocket Logic” system allows you to securely link your investment accounts (Fidelity, Vanguard, Charles Schwab) directly to the application.

- The Senior Benefit: This eliminates the need to fax, scan, or hunt for hundreds of pages of bank statements. Their system verifies your “Ability to Repay” instantly using your assets, often providing a verified approval letter in minutes rather than weeks. This speed is crucial in a competitive housing market.

3. Best for Complex Situations: CrossCountry Mortgage

Sagewise Rating: 4.5

- Why it wins: Sometimes, a computer algorithm will say “No” because your income looks messy. You might have a small pension, some rental income, dividend payouts, and Social Security. CrossCountry is known for Manual Underwriting, where a human being reviews your file to understand the full picture.

- The Senior Benefit: If you have a unique mix of income streams that confuses automated systems, their loan officers can manually build the case for your approval. They are often willing to look at “compensating factors”—like a high credit score or low debt—to approve loans that big banks reject.

4. Best for Banking Customers: Chase Bank

Sagewise Rating: 4.5

- Why it wins: If you already bank with Chase, they offer Relationship Pricing. This is a massive perk for seniors who have consolidated their savings.

- The Senior Benefit: They often knock 0.125% to 0.50% off your mortgage interest rate if you hold significant deposits or investments with them. For a senior who just sold a home and has cash sitting in the bank, this rate reduction can save thousands of dollars in interest over the life of the loan. It rewards you simply for keeping your money where it is.

5. Best for Reverse Mortgage Options: Fairway Independent Mortgage

Sagewise Rating: 4.0

- Why it wins: Fairway is a massive lender that has a dedicated, highly-rated Reverse Mortgage Division. Unlike some lenders who “dabble” in it, Fairway has certified specialists.

- The Senior Benefit: Many seniors aren’t sure if they want a traditional mortgage or a Reverse Mortgage. Fairway can quote you both side-by-side. They are one of the top HECM lenders in the nation and can help you execute a “HECM for Purchase,” allowing you to buy a new retirement home with about 50% down and never make a monthly mortgage payment.

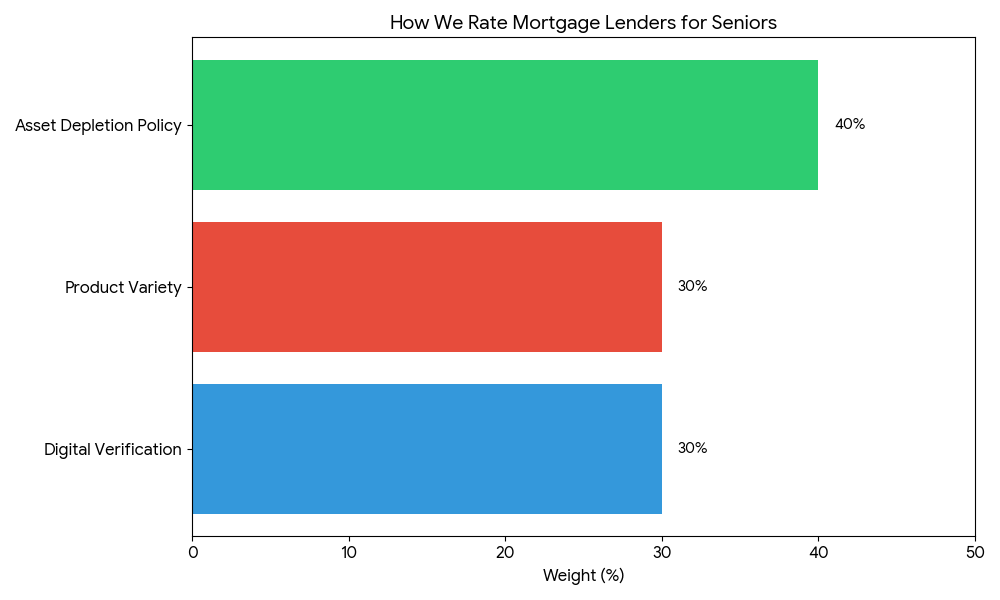

How We Rate Mortgage Lenders for Seniors

We don’t care about flashy Super Bowl ads. We care about underwriting flexibility. A lender is useless to a retiree if they only look at W-2 income.

- Asset Depletion Policy (40%): Does the lender have a clear, simple formula for using your savings as income?

- Digital Verification (30%): Can they verify your Social Security and Pension electronically, or do they make you hunt for award letters?

- Product Variety (30%): Do they offer 15-year, 30-year, and Reverse Mortgages? You need options.

Frequently Asked Questions (FAQ)

Yes, but only with the right lender. This is called Asset Depletion. Most lenders will take 70% of your account balance and divide it by 360 months to create a “phantom income” for qualification.

Yes. In fact, it counts more than regular income. Because it is often tax-free, lenders can “gross up” your Social Security by 125%. If you get $2,000/month, the bank treats it like $2,500/month.

There is no maximum age. The Equal Credit Opportunity Act forbids age discrimination. You can get a 30-year mortgage at age 90 if you have the income and credit score.

Online lenders (like Rocket or Guaranteed Rate) are often better for retirees because they have more sophisticated technology to verify non-traditional income sources. Local banks may have stricter, old-fashioned rules.

No, the requirements are the same. A score of 620+ works for conventional loans, but 740+ gets you the best rates. (See our Credit Score Guide).

Get Your Mortgage Quote (Find a lender who understands retirement income today.)