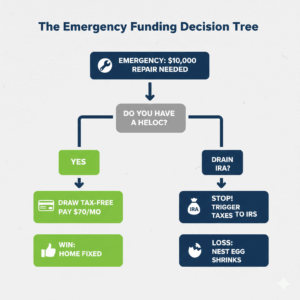

When a major home emergency strikes—a $10,000 roof leak, a $6,000 furnace failure, or a $4,000 main line plumbing clog—most seniors have two choices: pull money from their IRA/401(k) or use Home Equity.

On the surface, using your “own money” in your IRA feels safer. You don’t want another monthly bill, and you’ve spent a lifetime saving for a “rainy day.” But in the eyes of the IRS, that rainy day comes with a steep price tag. Because Traditional IRA withdrawals are taxed as ordinary income, taking $10,000 to fix a roof could actually cost you **$12,500** once the IRS takes its cut. Worse, that extra income can trigger a chain reaction that makes your Social Security benefits taxable and potentially raises your Medicare premiums.

As your trusted advocate, we are here to act as your financial bodyguard. We will show you why a Home Equity Line of Credit (HELOC) is the ultimate “emergency fund” for seniors and how to use it to protect your nest egg from a massive tax bill.

Key Takeaways

- The Tax Shield: IRA withdrawals increase your taxable income; HELOC draws are 100% Tax-Free loans.

- Preserving Growth: Keeping your $10,000 in the market allows it to continue compounding, while the HELOC interest rate is often lower than historical investment returns.

- The Deduction Advantage: Unlike debt consolidation, using a HELOC for home repairs makes the interest 100% Tax-Deductible (if you itemize).

- The Strategy: Use the HELOC for the “Shock” of the repair, then pay it back slowly using your monthly Social Security check or future Required Minimum Distributions (RMDs).

Don’t let a leaky roof drain your retirement. Repair your home safely. 👉 Explore Debt Relief Options

The Hidden Tax Advantage of Using Home Equity

Choosing a HELOC over an IRA withdrawal essentially comes down to Tax Avoidance. When you withdraw funds from a traditional IRA, you are creating “Provisional Income.” If that withdrawal pushes you over the IRS threshold, the government can tax up to 85% of your Social Security check (The “Tax Torpedo”). A HELOC draw is a loan, not income. The bank sends you tax-free cash, and you maintain your lower tax bracket, saving you thousands in hidden costs and preserving the longevity of your retirement accounts.

The Math: IRA Withdrawal vs. HELOC Draw

Let’s look at the real cost of a $10,000 emergency repair for a senior in the 22% tax bracket.

|

Cost Component

|

IRA Withdrawal Path

|

HELOC Draw Path

|

|---|---|---|

|

Initial Cash Needed

|

$10,000

|

$10,000

|

|

Federal Income Tax

|

**$2,200** (Owed in April)

|

$0 (Tax-Free)

|

|

SS Tax Impact

|

High (Likely triggers tax)

|

Zero

|

|

Interest Cost (1 Year)

|

$0

|

~$850 (at 8.5% rate)

|

|

Portfolio Opportunity Cost

|

Lost growth on $12,200

|

**$0** (Money stays invested)

|

|

Total Out-of-Pocket

|

$12,200 + Lost Growth

|

$10,850

|

The Verdict: By using your IRA, you “burned” at least $1,350 more than you needed to. The HELOC allows you to leverage your home’s value to keep your cash where it belongs: earning interest for you.

The "Tax Torpedo" Risk: A Warning for Seniors

If you are searching for “how to avoid taxes on IRA withdrawals,” you must understand the interaction between your income and your Social Security. As we discussed in our guide on Social Security Taxability, the IRS uses a formula called “Combined Income.”

- The Trigger: A $10,000 IRA withdrawal for a roof counts as 100% income.

- The Result: This can push you into the “85% taxable” tier for your benefits.

- The Cost: You might end up paying taxes on your Social Security for the first time ever, simply because you fixed your house. Using a HELOC avoids this entire trap because loan proceeds are never counted toward “Combined Income.”

The "Aging-in-Place" Upgrade Secret

If you are using equity for a repair, consider adding a “Safety Upgrade” at the same time. This is the smartest way to use your Home Equity to stay in your home longer.

- The Logic: If a plumber is already at your house fixing a main-line leak, the labor cost to add a walk-in tub or grab bars is significantly lower than a standalone project.

- The Benefit: These modifications prevent falls, which are the #1 cause of seniors losing their independence. By using a HELOC to make your home safer, you avoid the $5,000+ monthly cost of an assisted living facility.

Consumer Protection: The "Three-Day Right of Rescission"

If you sign a contract with a high-pressure roofer or contractor and realize you’ve made a mistake, remember the law is on your side. Under the FTC’s Cooling-Off Rule, you have three business days to cancel a home improvement contract or a HELOC agreement without penalty.

Bodyguard Action Plan: If you feel “buyer’s remorse,” send a written cancellation notice immediately via certified mail. Do not let a contractor bully you into a “same-day deal” for a major repair.

Frequently Asked Questions (FAQ)

Yes, but you must be careful. Most lenders require an “Exterior Appraisal.” If the roof looks visibly “distressed” or has a tarp on it, they may deny the loan until it is fixed. The Strategy: Get your HELOC set up before the emergency happens so the “ATM” is ready when the storm hits.

Yes. Under the Tax Cuts and Jobs Act, interest on home equity debt is deductible if the funds are used to “buy, build, or substantially improve” the home that secures the loan. Fixing a roof or HVAC system qualifies as a “substantial improvement.”

Most senior-friendly lenders look for a 660 score, but you can get a Personal Home Improvement Loan with a score as low as 600. Keep in mind that a lower score will result in a higher interest rate.

No. Unlike IRA withdrawals, which can trigger an IRMAA surcharge (higher Medicare premiums) two years later, a HELOC draw is not “Modified Adjusted Gross Income” (MAGI). It has zero impact on your healthcare costs.

This is the critical risk. A HELOC is a mortgage. If you default, the bank can initiate foreclosure. Never use your home equity for repairs unless you have a clear plan to pay the monthly interest—even if that means using a portion of your Annuity Payout or Social Security.

Explore Debt Relief Options (Fix your home and protect your taxes today.)