If interest rates drop even slightly, mortgage lenders will start calling you. They’ll promise to “Lower your rate by 1%!” and save you hundreds of dollars a month. For a senior on a fixed income, $200 back in your pocket sounds like a miracle—a way to fight inflation or cover rising Medicare Part B premiums.

But for a retiree, the interest rate isn’t the most important number. The most important number is the Break-Even Point.

Refinancing is only a winning strategy if the Monthly Savings will pay back the Closing Costs within 24 to 36 months. At age 75, your “time horizon” is shorter than a 30-year-old’s. If the math shows it takes 5 years to break even, and there’s a chance you might downsize, move to assisted living, or pass away before then, the bank is the only one winning. Refinancing is not free; it typically costs $3,000 to $6,000 in appraisal fees, title insurance, and taxes. If you pay $5,000 to save $100 a month, you have actually lost $1,400 if you move in three years.

As your trusted advocate, we are here to act as your financial bodyguard. We will show you the simple math to see if a refi is a gift or a trap for your 2026 budget.

Key Takeaways

- The Golden Rule: Only refinance if you plan to stay in the home longer than it takes to recover the upfront costs.

- The “Reset” Trap: Beware of resetting a 15-year mortgage back to 30 years; it lowers your payment but triples your total interest.

- The 1% Threshold: Most experts suggest a rate drop of at least 0.75% to 1% is needed to justify the administrative fees.

- The Alternative: If you just want a lower payment without the fees, ask about a Mortgage Recast.

The Anatomy of Closing Costs: What are you paying for?

Seniors are often shocked to see a $5,000 bill for “paperwork.” Lenders are required by the Consumer Financial Protection Bureau (CFPB) to give you a Loan Estimate within three days of your application. Here is where that money actually goes:

|

Fee Type

|

Typical Cost

|

Why Seniors Pay It

|

|---|---|---|

|

Appraisal Fee

|

$500 - $700

|

The bank must verify your home hasn't lost value since you retired.

|

|

Title Insurance

|

$1,000 - $2,000

|

Protects the lender (and you) against old liens or ownership disputes.

|

|

Origination Fee

|

0.5% - 1.0% of loan

|

The "commission" the bank takes for processing the new loan.

|

|

Credit Report Fee

|

$50 - $100

|

Verifying your senior credit score hasn't dipped.

|

|

Recording Fees

|

$100 - $300

|

Paid to the county to update the deed records.

|

The Bodyguard Warning: If a lender says there are “Zero Closing Costs,” they are likely rolling that $5,000 into your loan balance. You are still paying it—with interest—for the next 30 years.

The Break-Even Math Table

Use this table to find your “Danger Zone.” If your scenario falls in the bottom row, hang up the phone on that lender.

|

Closing Costs

|

Monthly Savings

|

Months to Break Even

|

Bodyguard Verdict

|

|---|---|---|---|

|

$4,000

|

$200

|

20 Months

|

SAFE (Great Move)

|

|

$4,000

|

$100

|

40 Months

|

CAUTION (Only if staying 5+ yrs)

|

|

$6,000

|

$80

|

75 Months

|

DANGER (The Bank Wins)

|

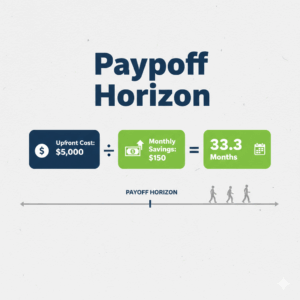

The Payoff Horizon

In this example, every month you stay in the house AFTER Month 34 is “pure profit.” Every month you leave BEFORE Month 34 is a “net loss.”

Retirement Stress Test

Will the new mortgage payment help or hurt your long-term stability? Use our Retirement Stress Test to see how your cash flow changes after accounting for the upfront fees and the new monthly bill.

The 15-Year vs. 30-Year Choice: The "End Date" Reality

If you are 70, do you really want a 30-year mortgage that doesn’t end until you are 100?

- The 30-Year: Offers the lowest monthly payment. This is the best choice if your only goal is maximizing your monthly Social Security check for daily living.

- The 15-Year: Offers a higher monthly payment but a much lower interest rate. You will save tens of thousands in interest and actually own the home free-and-clear while you are still active.

Bodyguard Tip: If you can afford the higher payment, the 15-year is the “Wealth Builder.” If your budget is tight, the 30-year is your “Safety Valve.”

Strategic Alternatives for Seniors

Before you commit to a full refinance, consider these two senior-specific tools:

- Mortgage Recasting: If you have a lump sum of cash (e.g., from an RMD or inheritance), you can pay down your balance and ask the bank to “re-amortize” your payment. This lowers your monthly bill for a flat fee of ~$250, without the $5,000 refi cost.

- Reverse Mortgage (HECM): If you are age 62+ and your primary goal is eliminating the mortgage payment entirely to increase your lifestyle, a Reverse Mortgage is often superior to a refinance.

Frequently Asked Questions (FAQ)

Yes. Lenders use a “Gross-Up” method where they count your tax-free Social Security income as being worth 125% of its value to help you meet their debt-to-income requirements.

Initially, yes. The lender performs a “Hard Inquiry,” which usually drops your score by 5-10 points. However, if the lower payment reduces your overall debt-to-income ratio, your score will typically bounce back and potentially even rise within 6 months.

Generally, no. A mortgage refinance is a change in the debt on the property, not a change in the ownership or assessment. However, some states trigger a re-assessment on any title change, so check with your local assessor’s office first.

Yes. This is a common move for seniors. However, remember that you are turning “unsecured” medical debt into “secured” home debt. If you miss payments, you risk foreclosure. A Personal Loan for Consolidation might be safer.

Expect a refinance to take 30 to 45 days. You will need to provide your SSA-1099 and pension statements to prove your retirement income stability.

Explore Debt Relief Options (Find the right path to a lower mortgage and a more secure retirement today.)