When a bank advertises a Home Equity Line of Credit (HELOC), they always lead with the “Interest-Only” payment. They’ll tell you that you can borrow $50,000 for just **$250 a month**. To a senior on a fixed income, that sounds like a manageable dream—a low-cost way to fix the roof or pay off high-interest credit cards.

It is the ultimate “Interest-Only Mirage.”

What the glossy brochures don’t emphasize is that this low payment is temporary. A HELOC is a “tale of two loans.” For the first decade, it feels like a low-cost safety net. But the moment the clock hits Year 11, the “Draw Period” ends, and the bank demands its principal back. For many retirees, this sudden spike in monthly obligations is a financial catastrophe that leads to the forced sale of their home.

As your trusted advocate, we are here to act as your financial bodyguard. We will explain exactly how to spot this trap, provide the math behind the “Payment Shock,” and give you a 10-year strategy to ensure your home remains yours.

Key Takeaways

- The Draw Period: Typically 10 years where you only pay interest. Your balance never goes down during this time.

- The Repayment Phase: Usually years 11-30. Your payment triples because you must pay back the full principal plus interest.

- The Variable Risk: Most HELOCs are tied to the Prime Rate. If the Federal Reserve raises rates, your “low” payment goes up automatically.

- The Strategy: Treat a HELOC like a standard loan from Day 1 by paying principal, or consider a Reverse Mortgage to eliminate payments entirely.

Don’t get caught by surprise payments. Lower your monthly costs safely.

Explore Debt Relief Options

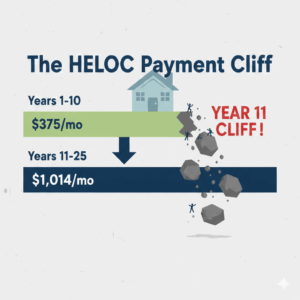

The "Payment Shock" Breakdown: Year 10 vs. Year 11

To understand the danger, you must look at the math of amortization. During the first 10 years (The Draw Period), your payment is calculated only on the interest. In Year 11 (The Repayment Period), the bank recalculates the payment to ensure the entire loan is paid off in the remaining 15 or 20 years

The Math of a $50,000 Balance (at 9% Interest):

|

Feature

|

Draw Period (Year 10)

|

Repayment Period (Year 11)

|

|---|---|---|

|

What You Pay

|

Interest Only

|

Principal + Interest

|

|

Monthly Bill

|

$375.00

|

$1,014.27

|

|

Total Debt Left

|

$50,000 (No change)

|

Decreasing monthly

|

|

Verdict

|

Affordable Mirage

|

Budget-Buster

|

The Shock Factor: In this common scenario, your monthly housing cost increases by $639.27 overnight. For a senior relying on a Social Security check that only increases by small COLA adjustments each year, this increase can consume 30% to 50% of their total monthly income.

The HELOC Payment Cliff

Retirement Stress Test

Can you afford a $600 monthly increase in your expenses? Use our Retirement Stress Test to see what happens to your “safety margin” if your HELOC payments double or triple in the future.

The "Prime Rate" Trap: Why Your Rate Never Stays Put

Unlike your primary 30-year fixed mortgage, a HELOC is almost always a Variable Rate loan. It is tied to the Federal Prime Rate, which is influenced by the Federal Reserve’s decisions to fight inflation.

- The Link: Most HELOCs are “Prime + 1%.” If the Prime Rate is 8.5%, your rate is 9.5%.

- The Danger: If the economy changes and the Prime Rate hits 12%, your payment goes up even during the interest-only phase.

- The Bodyguard Tip: Before you sign, ask for the “Lifetime Cap.” This is the legal maximum interest rate the bank can charge you. If the cap is 18%, you must ask yourself: “Could I afford this loan if the rate hit 18%?” If the answer is no, the loan is too risky for your retirement.

The "Frozen ATM" Risk: Stability Warning

As we discussed in our guide on the Secured Debt Trap, banks have the right to freeze or reduce your line of credit at any time if they believe your home value has dropped or your credit score has dipped.

Imagine you are counting on your HELOC to pay for an upcoming surgery in Year 8, only to find the bank has “turned off the tap” because the local housing market slowed down. This lack of guaranteed access makes the HELOC a poor choice for a primary emergency fund compared to a Fixed-Rate Personal Loan.

The 10-Year “Survival Strategy” for Seniors

If you already have a HELOC or are determined to get one, you must have a “Financial Bodyguard” plan to avoid the Year 11 cliff.

- Pay Principal from Day 1: Don’t let the bank tell you what to pay. If the interest is $250, send $500. This reduces the “shock” later by shrinking the balance before the repayment phase begins.

- The “Fixed-Lock” Feature: Many modern lenders (like BMO or PNC) allow you to “lock in” a portion of your HELOC balance at a fixed interest rate with a fixed term. This essentially turns part of your line of credit into a predictable home equity loan.

- Refinance Early: Do not wait until Year 10. In Year 7 or 8, look at moving the balance into a Cash-Out Refinance with a fixed 15-year term.

- The “Cash Unlock” Exit: If you are age 62+ and facing the repayment phase, a Reverse Mortgage can be used to pay off the HELOC. This eliminates the monthly payment entirely, protecting your cash flow for the rest of your life.

Frequently Asked Questions (FAQ)

Sometimes. Some banks allow you to “renew” the draw period for another 10 years, but this requires a full credit check and a new appraisal. If your income has dropped (retirement) or your home value has dipped, the bank may deny the extension, leaving you stuck with the higher payments.

Yes, banks are required by the Truth in Lending Act to send you a notice before the repayment period begins. However, this notice often arrives only 30-60 days before the spike—not enough time for most seniors to make a major financial pivot.

Only if the money is used to “buy, build, or substantially improve” the home. If you used the HELOC to pay off credit cards or medical bills, the interest is not tax-deductible. (See our guide on Senior Tax Deductions for more info).

If you miss payments during the repayment phase, the bank can initiate foreclosure. Because the loan is “secured” by your home, they have a direct path to taking the property. This is why we urge extreme caution when using home equity for daily expenses.

Check your most recent monthly statement. It should list the “Draw End Date.” If that date is less than three years away, it is time to sit down with a financial advocate to plan your exit strategy.

Explore Debt Relief Options (Find a stable, fixed-rate plan to protect your home and your income today.)